Are All Token Buybacks a Real Deal?

Intro

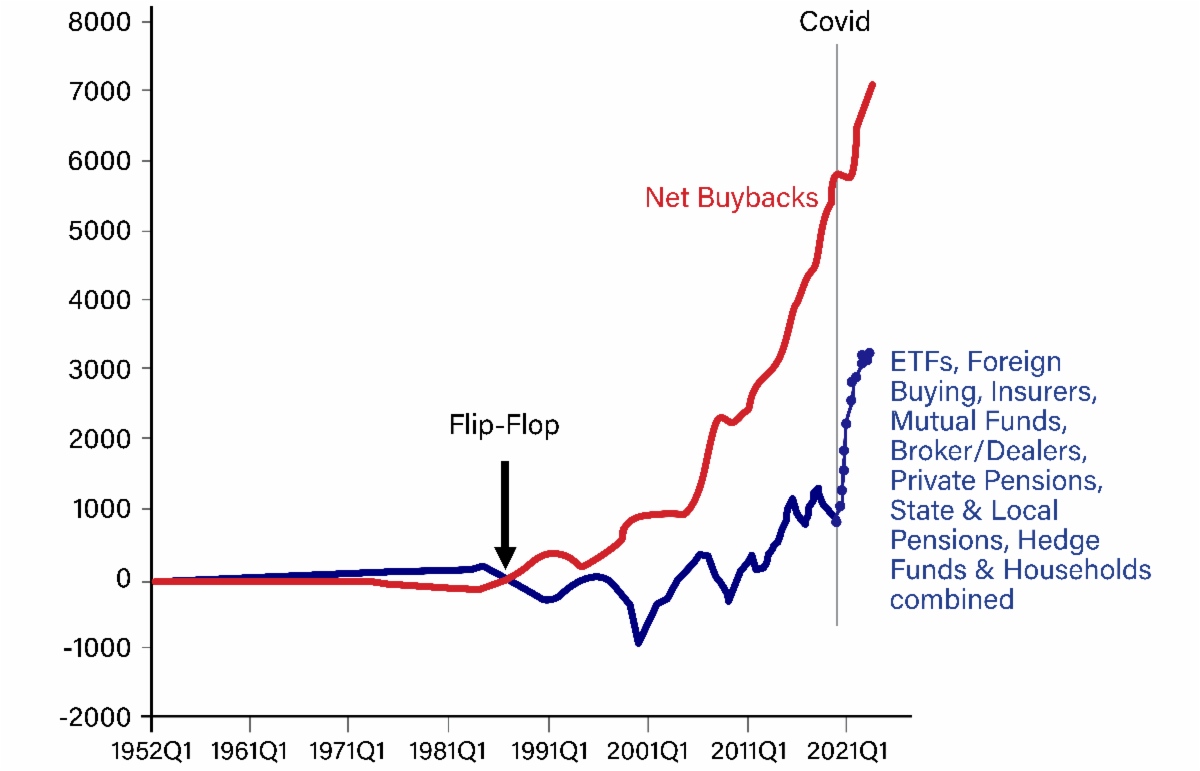

In traditional markets, buybacks are one of the most powerful levers a company can pull. When firms repurchase their own stock, they basically reduce supply, signal confidence, and often drive price appreciation. In fact, buybacks have been the single largest source of demand for equities over the past two decades, bigger than pensions, retail, and ETFs combined (!!!).

Now this tool is making its way into crypto. If designed well, on-chain buybacks could permanently reshape token price action, aligning incentives between protocols and holders while introducing a self-sustaining feedback loop of value capture. What Wall Street perfected for stocks, Web3 might just re-engineer for tokens, with even more transparency, programmability and composability.

To be fair, buybacks aren’t some shiny new thing in 2025; indeed plenty of crypto projects have been running them for years. What’s different now is the general mindset on the topic: Web3 is finally leaning into a Wall Street playbook, while TradFi itself is marching toward crypto with stablecoin regs opening the gates. It’s a real-time convergence. Layer on top the surge in DATs, the boom in crypto ETFs, big payment networks and merchant banks greenlighting on-chain payments, and consumer apps steadily growing: suddenly the outlook for this industry doesn’t just look positive, but rather unstoppable.

So let's take a closer look now at this booming new phenomenon and then understand how it has been implemented on chain, which projects are applying it, and which are moving in this direction.

A bit of context

For most of Wall Street’s history, stock buybacks were practically banned. Before 1982, they were treated as outright manipulation: a way for companies to unfairly goose their share price. That all changed when the SEC passed Rule 10b-18, giving firms a legal “safe harbor” to repurchase their own stock. From that moment on, the playbook of corporate America shifted forever.

Over the next ten years (1990 to 2000), buybacks slowly became from side tool to the main capital allocation strategy: instead of hoarding cash or locking into dividend commitments, companies realized they could shrink their float, boost EPS, and reward shareholders in a tax-efficient way, all while giving themselves flexibility to start and stop whenever they wanted (avoiding contemporary potential threats of hostile takeover).

Fast-forward to today, and buybacks aren’t just another factor in markets… they ARE the market.

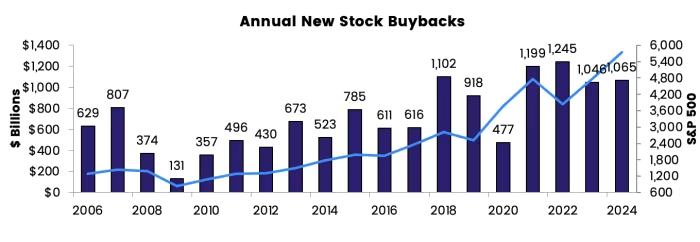

In many years, corporate repurchases have been the single largest source of equity demand, bigger than pensions, ETFs, retail, even foreign investors. In 2018 alone, buybacks hit $806 B, larger than the GDP of Switzerland. From 2010–2020, U.S. corporates were effectively the only net buyers of stock, pouring trillions into their own shares and keeping equity markets afloat.

If buybacks can reshape the world’s largest capital market, imagine what happens when this same mechanism becomes a native primitive in crypto.

An overview of existing solutions to date

What started as simple, TradFi-inspired supply reduction is now evolving into a whole toolkit of mechanisms, each with its own impact on demand, liquidity, and long-term alignment between protocols and their communities.

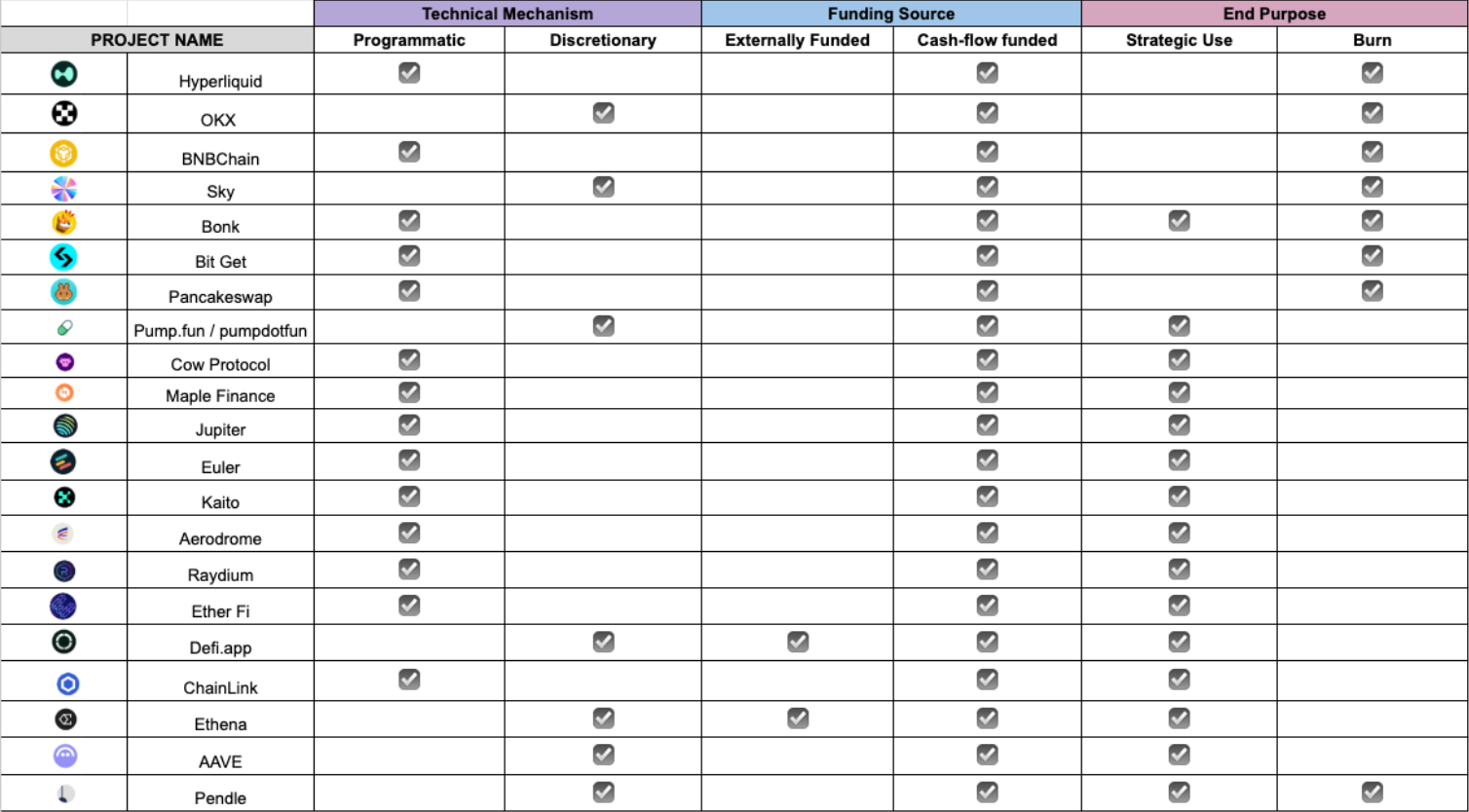

To really understand buybacks in crypto, we need to map them across 3 key axes:

1/ Timing mechanism

- Programmatic buybacks: fully automated, happening on-chain at defined intervals or thresholds.

- Hyperliquid sets the bar here: buybacks are literally block by block, feeding constant demand reflexively tied to activity.

- Jupiter and Raydium fall into this bucket too, allocating fixed shares of protocol fees (50% and 12%, respectively) toward automated buybacks.

- Discretionary buybacks: executed irregularly, usually after governance proposals or council decisions.

- Orca’s 24-month program gives its council authority to use 30% of protocol fees (held in the treasury) for buybacks, then decide whether to burn, redistribute as xORCA rewards, or fund ecosystem grants.

- Aave, Ethena, EtherFi, Chainlink also fall here with treasury-funded weekly/monthly buyback schedules.

2/ End purpose

- Deflationary (burns): the most aggressive design, permanently removing tokens from circulation.

- Sky (formerly MakerDAO) burns 100% of tokens it repurchases, shrinking supply by about 2% annually.\

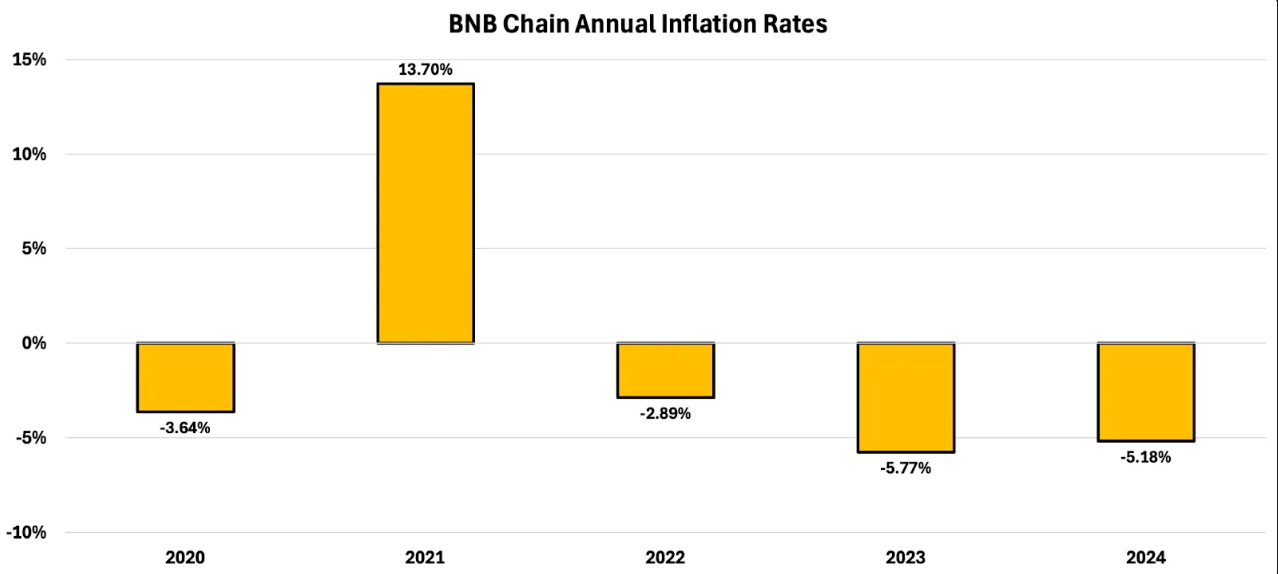

- BNB does the same at CEX scale, cutting circulating supply by more than 5% per year.

- Redistributive / strategic use: tokens are recycled back into the ecosystem to reinforce alignment.

- Orca (xORCA staking rewards + ecosystem grants) fits here.

- Euler creates a market-based loop that funnels external revenue back into its native token, while giving the DAO flexibility to decide how that value benefits the ecosystem. How? All fees collected from Euler vaults (in assets like USDC, DAI, etc) are periodically auctioned off to the public. The twist is that bidders must pay using EUL tokens. This guarantees that protocol revenue is consistently converted into EUL. The EUL collected is then sent to the Euler DAO treasury, where governance decides its ultimate fate: whether that’s burning tokens, redistributing them to stakers, or allocating them for incentives and growth.

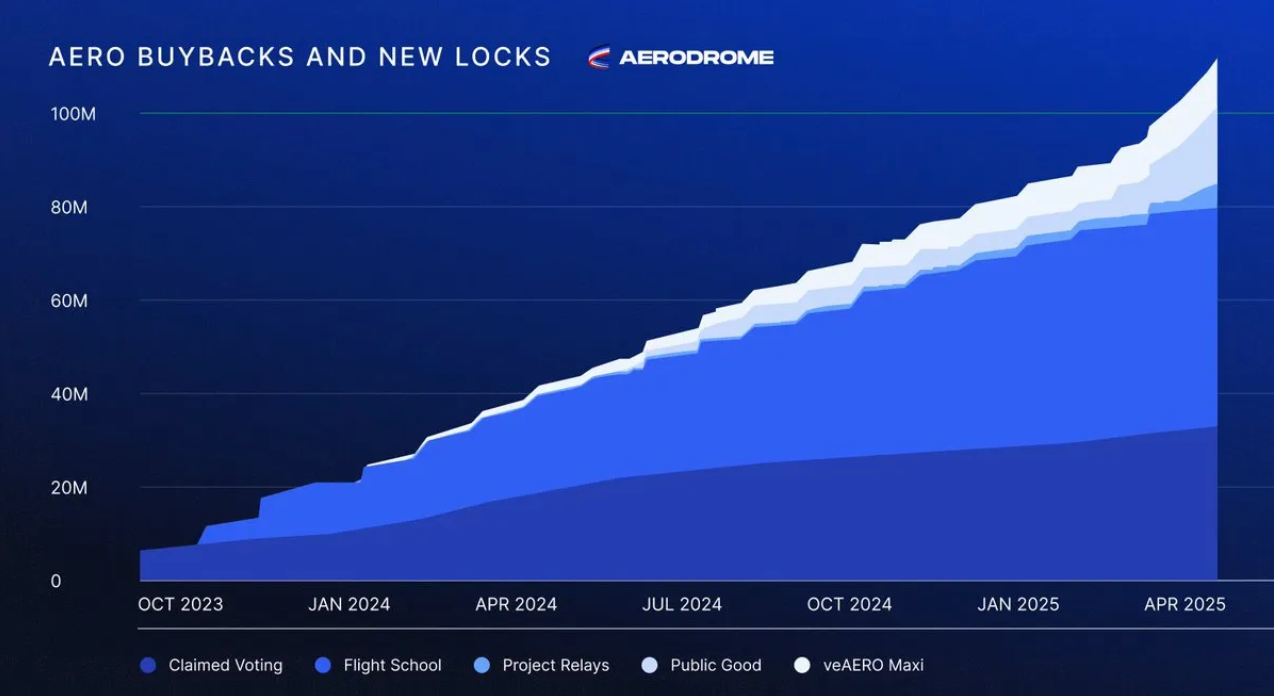

- Aerodrome allocates 30% of protocol revenue to buybacks but locks them as veAERO for 4 years, strengthening long-term alignment and reducing circulating supply.

- Cow DAO treasury uses a portion of revenue to buy back COW specifically for solver incentives (dynamically adjusted based on solver incentive requirements), which effectively makes token issuance/burn net neutral. The remaining revenue is retained in the treasury to ensure protocol sustainability and fund future growth initiatives.

3/ Funding source (the DAT axis)

This is the newest and most important lens: where does the money for buybacks actually come from?

- Cash flow–funded buybacks: directly powered by protocol revenue; the “earn and return” model. The vast majority of crypto projects actually belong to this category.

- Jupiter, Raydium, Hyperliquid, Maple, Pump.Fun (allocations set in predefined % of revenue generated).

- Euler, Aerodrome, Cow DAO (adaptive redistributive systems that recycle fees into native token demand or as an incentive support tool).

- Externally financed buybacks: not tied to current protocol earnings but treasury reserves or external capital, often raised through typical TradFi funding channels (e.g. through DATs).

- Arbitrum’s proposed bond-financed buyback program (using convertible debt to repurchase ARB from the market).

- OlympusDAO’s 2022 buybacks (funded by its treasury during the OHM contraction phase).

- Aave/Ethena/Chainlink (relying on treasury surpluses rather than immediate protocol revenue).

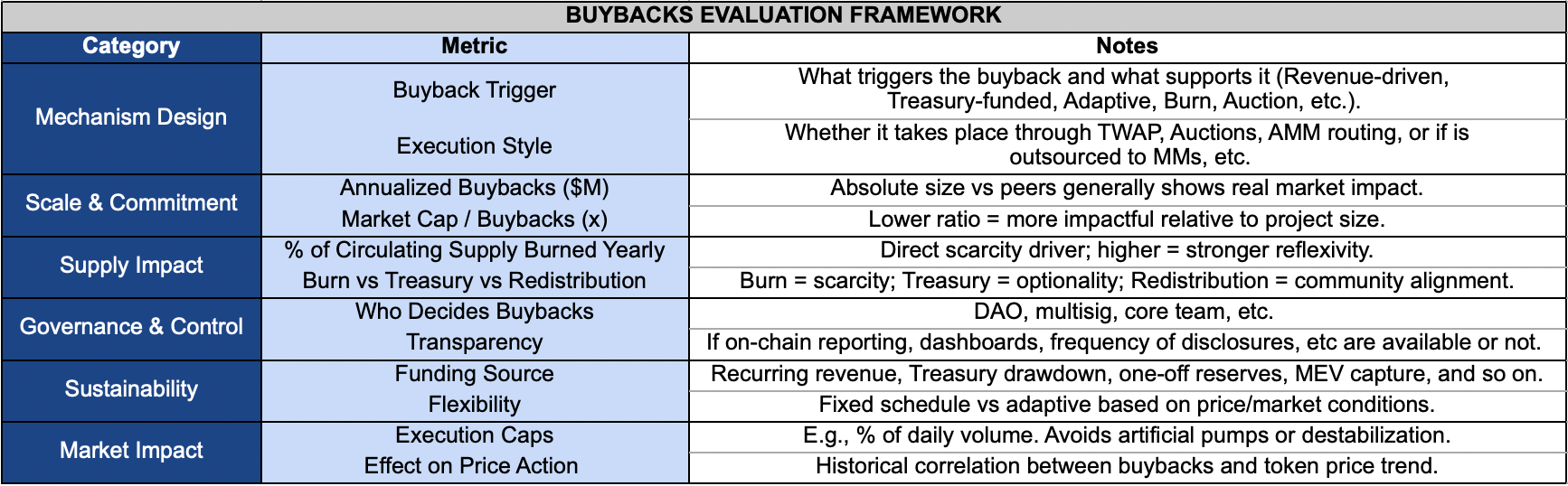

How to assess a buyback model

If token buybacks are going to be a defining force in Web3 tokenomics, then we need a clear way to separate the noise from the signal. Not every buyback program is indeed created equal: some are sustainable engines of value accrual, while others are little more than marketing activities.

That’s why we built a structured Buybacks Evaluation Framework: a set of categories and metrics to assess how impactful, sustainable, and aligned a given program really is. From mechanism design and execution style, to its supply impact, governance alignment, sustainability, and real market effect, these parameters let us benchmark different protocols and identify which buybacks are truly meaningful, and which are just kicking the can down the road.

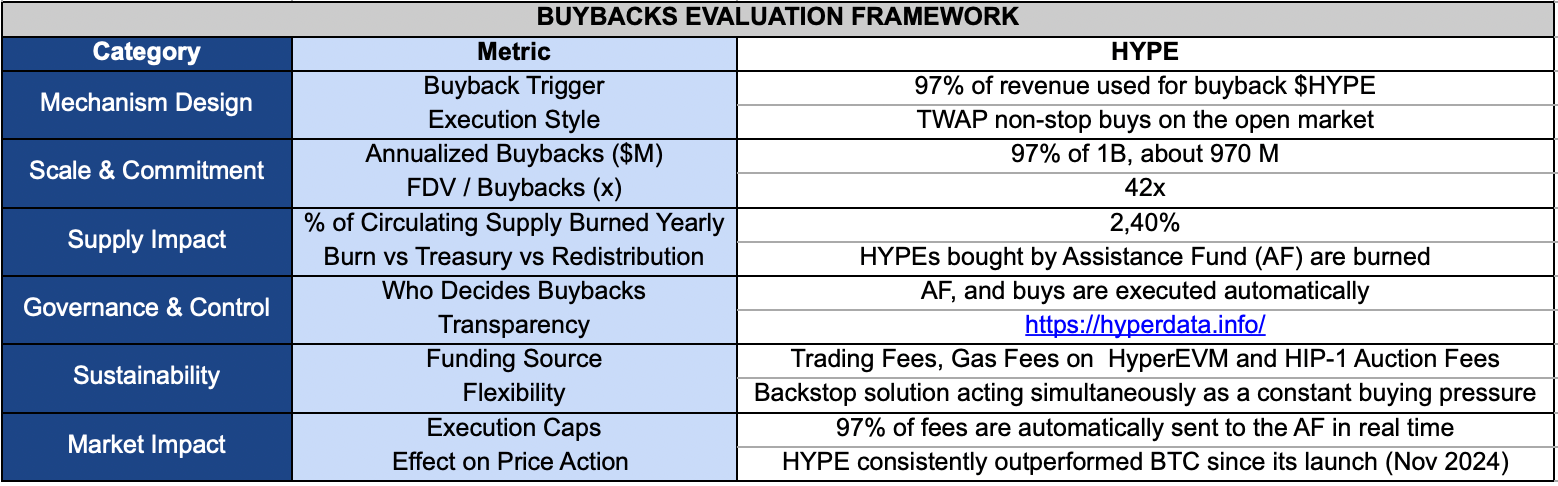

Let’s break down one of the most compelling case studies in the buyback arena, the project that’s arguably unlocked the full potential of this mechanism: Hyperliquid.

Which Projects Will Jump on Buybacks in the 2nd Half of 2025?

As we saw, buybacks are quickly becoming a core feature of tokenomics design in Web3. And the momentum is spreading fast. Several protocols have already announced (or are actively debating) governance proposals to adopt buyback frameworks in the second half of 2025. Here are some of the most notable names to watch:

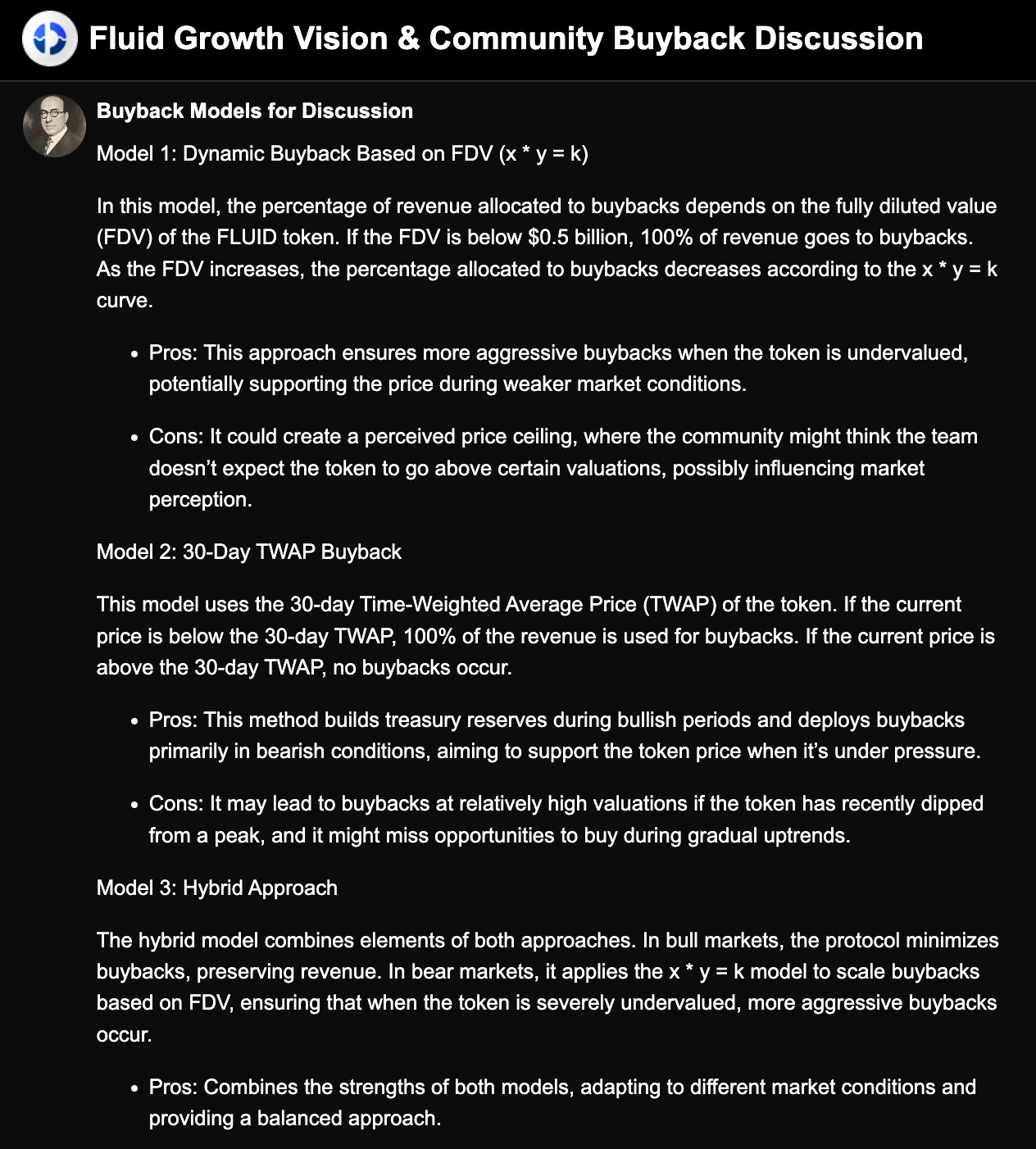

**Fluid.** Governance is weighing these days (21/08/25) 3 distinct frameworks:

- Model 1: Dynamic Buyback (x * y = k).Buyback intensity scales inversely with valuation. If FDV is <$500M, 100% of revenue goes to buybacks. As valuation rises, allocation decreases. This approach ensures aggressive support when the token looks undervalued but could also set a “psychological ceiling” if the market reads the curve as implicit valuation guidance.

- Model 2: TWAP-Triggered Buybacks.Uses the 30-day TWAP as a benchmark. If $FLUID trades below it, revenue flows to buybacks. If above, revenue is preserved in treasury.It could miss gradual uptrends, or lead to late buys after sharp dips.

Model 3: Hybrid.Combines both approaches: conservative in bull markets, aggressive in bear conditions. It seems the most balanced, aligning treasury strength with opportunistic repurchases.

**Jito.** Jito is moving fast toward cementing buybacks as part of its economic engine. With JIP-24, the DAO now receives the entirety of Block Engine fees, plus future fees from the newly launched Block Assembly Marketplace (BAM), a design space that introduces plugins for programmable, value-accretive blockspace. All of these flows are routed straight to the DAO treasury, with the CryptoEconomics SubDAO (CSD) tasked to deploy them into tokenholder-facing value accrual mechanisms. In other words, the revenue that used to be split between Jito Labs and the DAO is now fully redirected to $JTO holders, and future BAM fees could add millions more annually. The plan is for these revenues to be recycled into buybacks, burns, or other accrual programs, making de facto $JTO one of most revenue-aligned tokens in Solana.

**Orca.** Orca governance has approved a proposal stating that 30% of protocol fees that flow into the Treasury Wallet (currently holding 55K SOL and $400K USDC) will be redeployed into two key initiatives:

- Validator Staking. Treasury SOL will first be staked to a dedicated Orca Validator, both to earn yield and to speed up transaction propagation for Orca users.

- DAO Buyback Program. Over the next 24 months, the Council can use treasury SOL and USDC to buy ORCA tokens on the open market (capped at 2% of average daily volume to avoid heavy market impact).

The repurchased tokens will be held in the DAO Treasury and can then be:

- Burned to permanently cut circulating supply,

- Distributed as extra xORCA staking rewards, or

- Used as ecosystem grants to fund growth.

To manage risk, buybacks pause during periods of high volatility (swings >15% in 24h), and quarterly reports will keep tokenholders updated on progress.

**Arbitrum.** The Arbitrum DAO is exploring one of the boldest buyback strategies in crypto: a debt-financed $ARB buyback program. Instead of relying solely on treasury funds, the DAO would issue zero-coupon convertible bonds: a financing tool often used in TradFi to raise capital through institutional investors.

The proceeds would then be used to systematically repurchase $ARB from the open market, with much of the acquired supply permanently retired and some potentially set aside for ecosystem incentives.

The model mirrors MicroStrategy’s debt-backed Bitcoin buys and is designed to:

- Create sustained buy pressure on $ARB,

- Reduce circulating supply of nearly 5B tokens,

- Transform treasury management from passive to active value creation, and

- Send a strong institutional signal of long-term conviction in the Arbitrum ecosystem.

If executed, this would mark the first large-scale institutional-style, bond-funded buyback in Web3, setting a precedent for other DAOs.

**Marinade.** Marinade Finance recently approved a landmark governance proposal (MIP-11) that channels 100% of protocol fees into the DAO treasury. Half of this revenue is earmarked for open-market $MNDE buybacks, a massive shift in tokenomics that positions Marinade as one of the most aggressive buyback adopters in the Solana ecosystem.

When a crypto project should consider buyback

It’s important to keep in mind that buybacks alone are not enough to sustain price action in the long run. They can never replace the core pillars of any startup: product–market fit, scalability, a validated business model, go-to-market execution, community growth, and the team’s ability to execute.

A buyback strategy only makes sense once a project has achieved real economic maturity: stable cash flow, a clear product, and deep enough liquidity to avoid distorting markets. At earlier stages, most teams need every dollar to reinvest in product development, expand use cases, and grow communities. If scarce treasury funds are diverted to buybacks too early, the project risks running out of steam. Tokens may see a short-term pump, but without competitive fundamentals, long-term value will erode.

Take a simple example: imagine an NFT marketplace with a $2M treasury at MVP stage. If it commits $500K to buybacks, the token might rally briefly. But with less capital left for R&D or growth, product innovation slows, user adoption stalls, and eventually the token bleeds out. Contrast that with a scenario where the full treasury is focused on PMF and scaling transaction volume. Once the marketplace generates steady fees, buybacks can then be powered by real cash flow, giving them true economic weight rather than serving as a temporary price gimmick. And not by chance, the first projects to ride this “new” narrative in 2025 are the same ones that generate a high and steady revenue stream (do Hyperliquid, Aave, Ethena and Jupiter ring a bell?).

So, when is the right time to launch buybacks? We can draw up a checklist:

- Stable cash flow. At least 2–3 quarters of profitability, with monthly revenue ≥ 1.5–2× burn rate.

- Market liquidity. Tokens should have daily trading volumes ≥ 20–30× the size of planned buybacks to avoid artificial pumps. If liquidity is thin, use TWAMM or similar tools to smooth execution.

- Healthy treasury. 60–70% of funds still reserved for R&D, growth, and incentives. Buybacks should represent <20% of treasury allocation, not the core strategy.

- Proven product and market. A clear PMF, loyal user base, and real traction. Buybacks should reward growth, not substitute for it.

- Clear objectives. Buybacks must be designed to share economic value with the community, not to manipulate short-term price action.

Conclusion

Buybacks in Web3 are not a gimmick borrowed from Wall Street: they’re the clearest signal yet that crypto is maturing into a capital market of its own. In equities, buybacks have become the single largest driver of shareholder demand, reshaping how companies return value. Now, with protocols experimenting across revenue-driven, treasury-funded, burn-based, and adaptive models, we’re watching the same logic take root, but with far more flexibility, composability, and transparency than TradFi could ever dream of.

The next wave of winners in crypto won’t just be those with flashy tokenomics or hype-driven launches, but likely the protocols hardwiring sustainable buyback mechanisms into their core design, creating reflexive flywheels where growth funds demand, and demand accelerates growth.

If designed right, buybacks could become the new gravity of token markets, anchoring value, amplifying conviction, and forcing a convergence between TradFi discipline and DeFi innovation.